Key Takeaways

Introduction

In 1995, buying (and paying for) ‘things’ online felt reckless; many users swore they’d never type a credit-card number into a browser. Today, we tap twice on a phone and think nothing of wiring rent across town. We’ve always underestimated the impact of platform shifts (PC, Internet, Mobile, Cloud, etc.) on delivery of financial services. However, these shifts have profoundly impacted Access, Experience, and Efficiency. As we approach the next platform shift, it seems certain that it will bring big changes across financial services.

Modern AI does two things its predictive forebears couldn’t: think like a knowledge worker and talk like a human. The first superpower is reshaping the operations of incumbent banks and financial institutions; the second will rethink how consumers engage with financial services. The corollary of this is two large opportunities for Indian startups and tech incumbents:

- Build AI platforms and services that will enable financial institutions to AI-supercharge their internal operations and processes

- Reimagine how financial services are delivered to customers

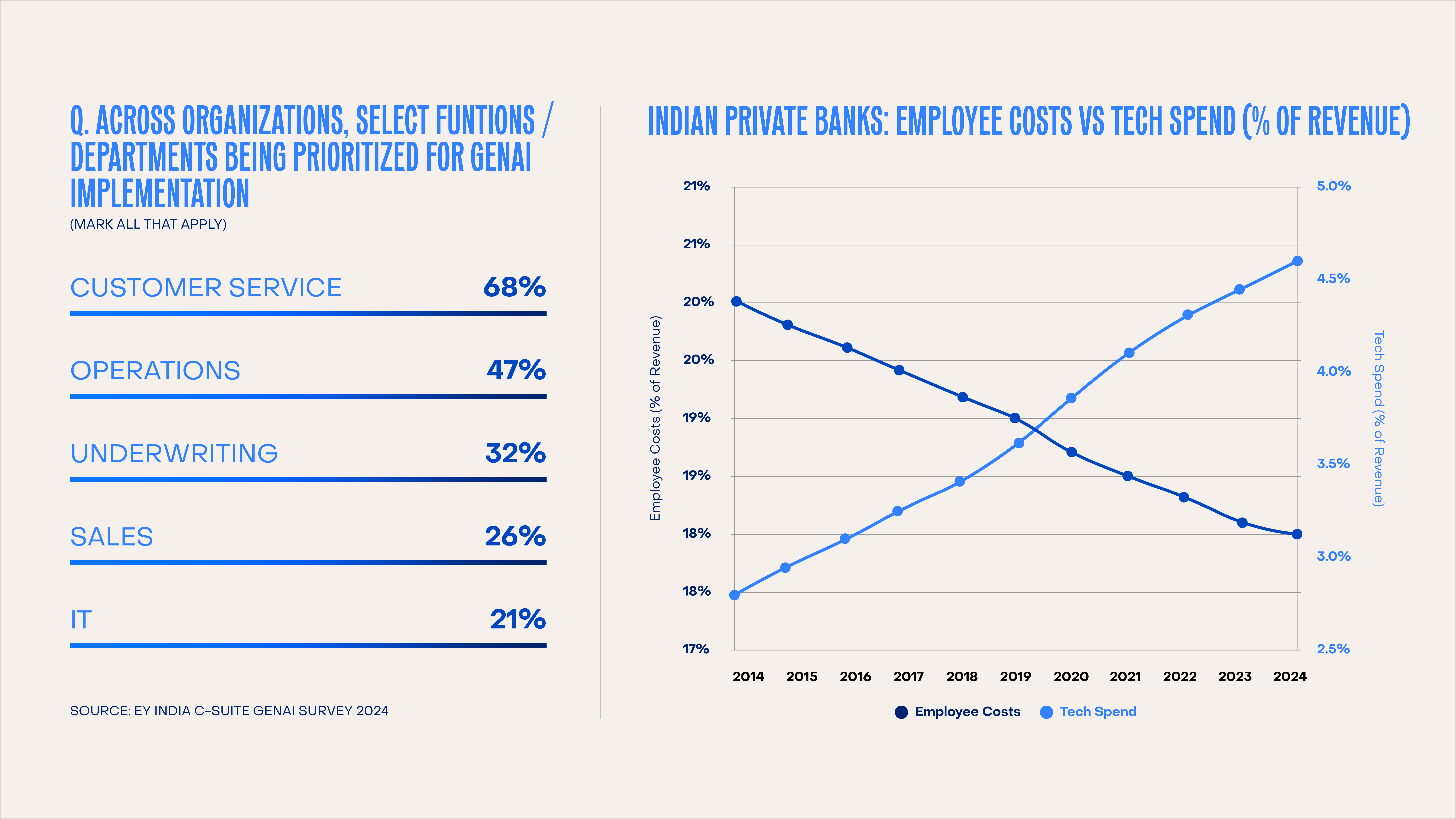

Financial institutions have been on a path of increasing digitization, thereby reducing manual and cumbersome tasks. Over the last decade, private banks in India have reduced employee spends as a percentage of revenue by 200bps (20% to 18%), with a concomitant increase in tech spends (2.8% to 4.6%). AI will inevitably supercharge this trend, and key executives are taking note. In a recent EY India survey on AI adoption priorities among financial services firms, 68% cited customer experience as the top transformation priority, followed by operations (47%), underwriting (32%), and sales (26%).

The Two Immediate Opportunity Areas

We are increasingly seeing AI adoption in the production environments of most large financial institutions, albeit for limited and simple use cases, such as monitoring call centers, soft collections, and simple regulatory reporting.

Based on current technical readiness and the nature of the task, we identify two immediate areas for AI adoption over the next 12-24 months: customer communication, and middle/back office automations in compliance, risk & credit operations.

However, adoption isn’t without hurdles. In conversations with senior leaders at large financial institutions, two challenges stand out. First, the sector’s unique demands around compliance, explainability, and customer trust are rarely addressed by generic AI solutions. Second, there’s a shortage of in-house talent to identify the right use cases, deploy effectively, and monitor outcomes. To address this, we’re seeing the rise of FS-specialized AI companies built from the ground up with domain-specific guardrails, explainability, and risk frameworks baked in.

We're seeing this thesis play out with companies in our portfolio. GreyLabs AI started with AI-powered speech analytics to automate audit/compliance checks and generate customer insights. Today, they process hundreds of millions of conversations for 50+ BFSI institutions. Their newly launched multilingual AI voice agents complete the stack – using insights from their analytics platform to power human-like AI calls for sales, servicing, collections, and more.

Fravity brings the same domain-first thinking to fraud and AML investigations. Their AI agents help BFSI ops teams investigate suspicious transactions in minutes, not hours. The impact is clear: 3x faster investigations with 2x better accuracy. What was once a manual, inefficient compliance burden for regulated entities is now an intelligent operation that can scale up volumes sustainably with Fravity’s agents.

The service delivery model itself is being reimagined by using Forward Deployed Engineers (FDEs), i.e., technical experts embedded within client teams. FDEs bridge the gap between abstract models and operational reality, helping clients move from unclear ambition to working AI systems, even in the absence of deep internal capabilities.

Bridging The Divide

From the customer's perspective, India’s financial services story is a curious mix of staggering digital success while still having a long way to go. Nearly 90% of Indian adults now hold a bank account, and UPI enabled 20 billion transactions in August 2025 alone, the largest real-time payment system in the world. However, large gaps remain in both access and experience. Insurance and wealth penetration is among the lowest in the world (insurance penetration in India is about 3.7% of GDP; mutual fund AUM as a percentage of GDP in India is around 19%), and more importantly, even for customers who have access to services, customer love hasn’t followed: average banking Net Promoter Score hovers around +30, among the lowest in any consumer category.

AI can close both the access and experience gap in a way that the first way of digitization couldn’t. Instead of tapping through menus and learning new interfaces, customers converse - by text, voice, or even vernacular video - with assistants that answer 24/7, learn individual preferences, spot intent in ambient data, and dispense advice without human biases or shift schedules. Think of it as moving from “click for service” to “talk like I’m your RM”, at population scale.

In a country with diverse languages and low financial knowledge, services delivered through voice (and video) could be a game-changer. We believe that voice AI, combined with deep personalization and autonomous operations agents, could allow a complete reimagining of how financial services are delivered – especially for complex products like insurance and investment products. We’re seeing glimpses of the future globally, as well as some experiments in India. Lemonade’s claims bot “AI Jim” pays ~40% of claims instantly, reframing consumer expectations for payouts.

Our portfolio company Acko has embedded AI end-to-end across multiple customer-facing and operational use cases: chatbots (24/7 personalized assistance), claims adjudication (faster processing, fewer errors), fraud detection (higher billing accuracy, reduced risk), dynamic pricing (fairer, more precise premiums), personalization (targeted offers and improved customer experience), and policy servicing (streamlined workflows, greater efficiency, and cost savings).

Similarly, Dezerv has built in-house AI tools that capture institutional memory of customers and automate repetitive manual tasks, enabling their wealth managers to deliver more personalized service at scale.

The Road Ahead

We don’t expect this change to happen overnight – even the mobile shift took a decade or two to play out. Regulators will scrutinize advice algorithms; customers must learn to trust synthetic voices with their money, and banks need robust guardrails against bias, hallucinations, and privacy violations. We expect an interim phase of AI-augmented workflows, where bots triage and humans close, before truly AI-native journeys emerge. The winners will be those who design for conversational finance, and not just add a voice or chat wrapper to previous form factors.

The AI wave is upon India, coinciding with the country's transition from a low-income to a middle-income nation. This presents a unique opportunity for both incumbents and new players to shape how financial services penetration happens in a manner that was hitherto impossible. When India reimagined payments in the mobile platform shift, we architected UPI – a system very different from those in other parts of the world. AI will likely do the same in the coming decade to numerous other financial products and services delivery.